There is no outperformance—or non-correlation—without differentiation. Yet investing differently in today’s market has never been scarcer.

Last year, nearly 60% of all new capital in private markets went to the industry’s six largest asset managers1. This level of overconcentration generates structural challenges for even the most capable funds, compressing returns as the available and scalable investment opportunities become limited or are outpaced by the velocity of capital accumulation. By definition, the majority of capital can’t be an outlier.

But average performance isn’t the only downside. If the crowd continues to cram too much capital into the same assets, then counterparty risks are created, bubbles are formed, and potential severe losses are created. The effects of this “Capital Cram” can already be seen in equities, private credit and bank lending.

How the “Capital Cram” Impacts Key Asset Classes

| Stocks | Private Credit (Non Asset-Based) | Bank Loans | |

|---|---|---|---|

| Evidence |

The top 10 stocks in the S&P 500 are now 35% of the index, a record high6. |

Covenant protections have been stripped to win deals while creditworthiness of borrowers deteriorates. |

Banks have >$1T in exposure to nonbank financial institutions5, including private credit players, potentially creating contagion risks. |

| Impact |

The S&P 500 has highest concentration risk ever. |

Only 7% of large private credit deals have covenants3. >40% of private lender borrowers had negative cash flow from ops4. |

“The fast growth and close connections between traditional lenders and nonbanks could add to systemic risk and future asset quality challenges.” – S&P Global, Feb 20255 |

If Direct Lending Private Credit Is This Concentrated, Should It Even Be Considered Alternative?

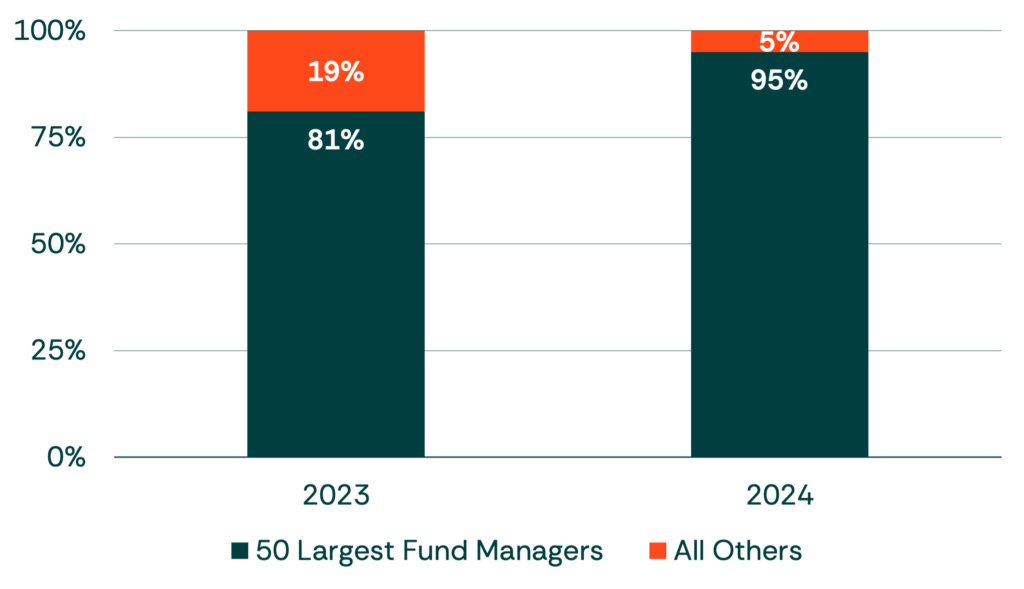

This effect is only increasing in private credit. In 2023, only 19% of all private debt fundraising went to fund managers outside of the top 50. By Q3 2024, that had plummeted to just 5%6. Direct lending, the largest asset class within private credit, is even more concentrated with the top 10 largest fund managers hold nearly half of all capital7.

Share of Private Debt Fundraising [6]

Amongst these top fund managers, there is also a rising amount of committed but uninvested capital—known as ‘dry powder’— potentially indicating that the supply of capital is exceeding the investment opportunity set. This volume and velocity of capital, and the pressure to deploy it quickly, can create a competitive race to the bottom in terms of return and risk protections, as seen in the table above.

Amidst this backdrop, one of the largest private debt firms released a public forecast to add $500B in AUM alone, driven primarily by direct lending.

Pursuit highlights these effects as potential warning signals. Ultimate impact on each sector, fund or asset could vary greatly.

Why Is This Happening?

The unspoken truth is that most large allocators are not incentivized to “take risks” on smaller or differentiated funds. Decision-makers who choose lesser-known managers over brand-name funds are risking their own careers—even if trying something new could ultimately be in their portfolio or client’s best interest. While these larger managers are highly respected, the contagion and systemic risks are growing.

This tension resembles the adage, “No one gets fired for buying IBM,” which was pervasive in the ‘60s and ‘70s. The difference is that IBM’s value proposition did not deteriorate as their market share grew. In contrast, we expect the risks of the “Capital Cram” to increase and accelerate alongside capital consolidation, revealing the hidden question in allocators’ “safe bets”: Which is the greater risk, the one you didn’t take or the one growing in plain sight?

The Differentiation of Niche Asset-Based Income

We encourage investors to consider these oft overlooked risks and ask themselves whether large, branded funds and crowded asset classes are the best fit for their capital. Diversifying even a portion of a portfolio can help mitigate risk.

At Pursuit Funds, we hope to offer a compelling, diversified, and idiosyncratic income stream through uncorrelated and hard-to-access niche investments in asset-based finance. We specifically target small, capital-starved markets that are overlooked by traditional lenders and larger funds.

We believe that by investing in niche assets, investors can take comfort that they are less exposed to the broader macroeconomic risks and “Capital Cram” that tend to create contagion, correlation and volatility.